|

October 18, 2006

A Gentle Reminder

Written by Jeff Thredgold, CSP, President, Thredgold Economic Associates

click here to read the full article from January 4, 2006

So there it is! The Dow Jones Industrial Average (the Dow) at an all-time high of 12000

just like we predicted on January 4

as my mother taught meIts better to be lucky than good anytime

The Dow set a series of new highs over the past two weeks. The Dow traded as high as 11997 on Monday. It gave ground on Tuesday of this week as the core Producer Price Index number was higher than expected.

The Dow average pierced the 12000 level today for the first time ever. The Dow actually traded as high as 12049 before backing off.

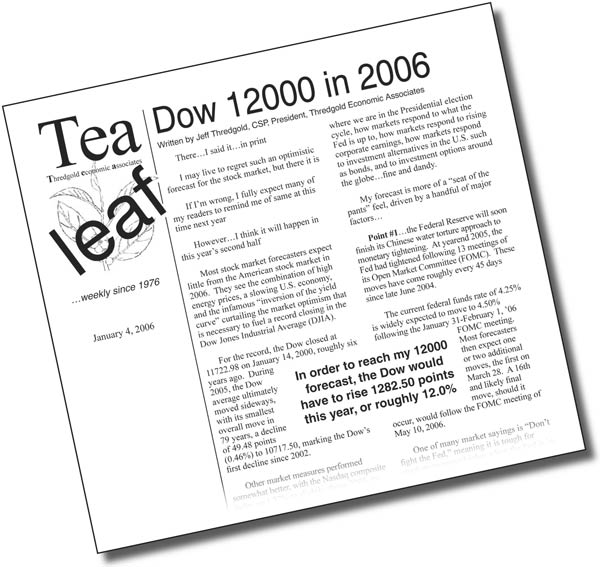

The graphic shown above is part of our Tea Leaf newsletter dated January 4, 2006. We noted four reasons at that time why the Dow average would not only break the all-time record of 11722 set in January 2000, but also trade above the 12000 level in 2006s second half

1. We noted that the stock market would respond favorably to the Federal Reserve concluding its Chinese water torture approach to monetary policy. We suggested on January 4 that the Fed would likely conclude its aggressive monetary tightening on May 16, 2006, with a 16th and likely final move to 5.00%

missed it by one

the Fed ultimately tightened 17 times, and has remained on hold since August 8. Financial markets currently expect the Fed to remain in pause mode through the end of the year. Financial market players currently expect one or two easing moves in the first 6-8 months of 2007. Note: Yes, there is still a camp of economists predicting that the Fed will feel compelled to tighten policy further in coming months to keep inflation pressures at bay

2. We noted that numerous foreign stock markets had outperformed U.S. markets in 2005, suggesting greater relative value within U.S. markets. We have seen various foreign markets struggle, while others have moved to 5-6 year highs

3. We noted that a rising awareness among 78 million Baby Boomers that we have not saved aggressively enough for retirement would lead savings and investment higher, with billions of new dollars earmarked for stock market investment. This has occurred and also remains a long-term issue, and is a key element supporting my view that the American stock market will do very well in coming years

4. We noted that billions of dollars would leave coastal and Southwestern real estate markets and be invested in the stock market, as further signs of a real estate bubble emerged. This should also drive stock prices higher in coming years

We concluded the piece with the following

These four points could also be supported with my view that A) U.S. economic growth in 2006 will be slightly above 3.0% after inflation, thereby leading to significant job and corporate earnings growth, and B) that I expect some additional relief in energy prices.

Friendly Data

Helping support stocks today was market-friendly housing data and somewhat market-friendly consumer inflation data. Housing starts actually rose 5.9% in September versus August, helping to refute the view of those forecasters who expect the demise of housing to lead the economy into recession.

In addition, consumer prices (the CPI) declined by 0.5% in September, led lower by the big drop in energy prices. We had noted in our Tea Leaf dated September 20 that the year-over-year measure of inflation would be much better with the September report.

Consumer prices have now risen a modest 2.1% over the past 12 months. This compares to a 3.8% year-over-year rise with the August data, a 4.1% rise when comparing July 2006 to July 2005, and an alarming 4.3% rise when comparing June 2006 versus June 2005.

Yes, the core CPI (which excludes volatile food and energy prices) remains of concern. The core rate was up 0.2% in September, with the year-over-year rise at a Fed-anxiety level of 2.9%. We do expect some moderation in the core rate over the next few months.

From Here?

I remain optimistic on where stocks go from here. Corporate profits have doubled during the past five years, a factor suggesting the market is solidly undervalued

stay tuned

Teasers

Headlines

Panda Mating Fails: Veterinarian Takes Over

Toilet Stolen

Police Have Nothing to Go On

Red Tape Holds Up New Bridges

Scott Friedman

|